For now, Canada is not in a recession — although fear of a shrinking economy is never far off in an era marked by Donald Trump and global disruption. And as a country, we’ve managed to eke out a smidgen of growth over the past year.

Since the pandemic ended, life for the wealthy has been a joyride. Financial markets have been soaring. The TSX has risen 87.5 per cent since January 2020. South of the border, the S&P 500 has risen 111.8 per cent during that same time period.

But since the pandemic ended, life for the rest of us has, more often than not, been a grind.

Your pay has inched ahead, but the high cost of housing and food claws back every bit of progress. Dreams of building wealth over time have been replaced with anxiety about slipping further behind, or about what will happen next to your job, your children or your holdings.

For now, Canada is not in a recession — although fear of a shrinking economy is never far off in an era marked by Donald Trump and global disruption. And as a country, we’ve managed to eke out a smidgen of growth over the past year.

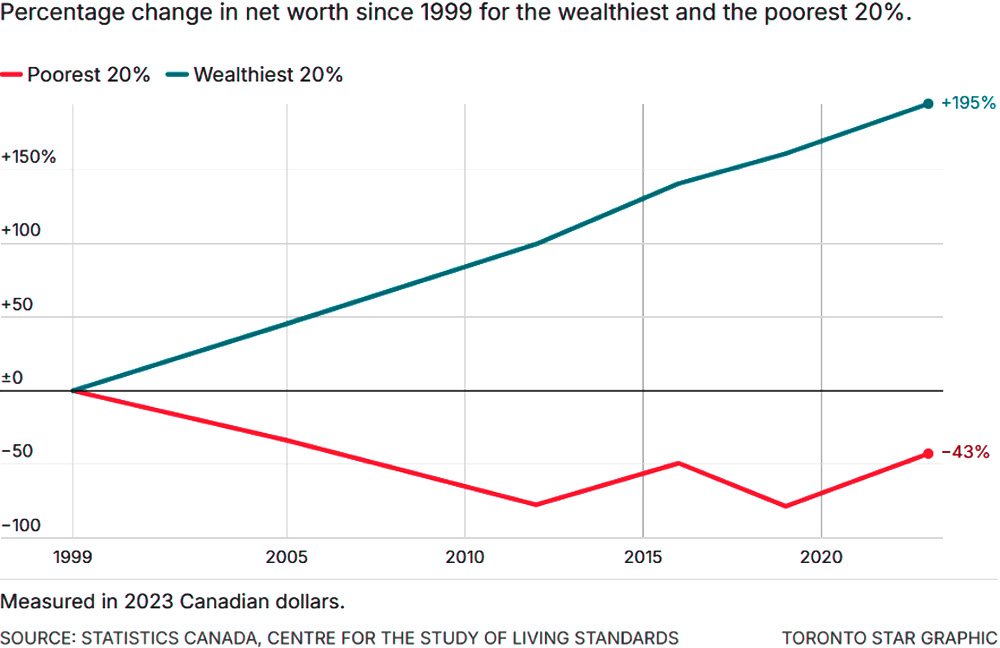

Changes in net worth for wealthiest and poorest

But Canada is in an economic predicament. We may have side-stepped the “R-word” for now but, instead, we have emerged from the pandemic into a troubling K-shaped recovery in which the wealthy prosper and millions of Canadians increasingly struggle. The effects of that change — and all that that pattern implies in terms of privilege and ease for a few, and deepening anxiety and hardship for others — go beyond mere statistics. They may well also be planting the seeds of envy, anger and deeper social unrest.

The “K” refers to the shape of lines on a graph of what the economy looks like over the past few years. The upper arm, representing the well-to-do, is on a roll. The lower arm typically groups together the rest of us, or zooms in on the least rich. For that group, it’s a picture of increasing hardship.

The wealth gap in Canada is long-standing, but in recent years it has widenined in a worrying way. Statistics Canada started keeping track of net worth by decile in 1999. Between that time and 2023, the top 10 per cent of wealthiest households in Canada have seen their net worth surge by 195 per cent. The bottom 10 per cent, on the other hand, has seen its wealth contract outright, by 43 per cent.

It’s a classic K.

And it is entrenched. To be sure, the pandemic shook up Canada’s economy and its growth patterns, but not this one. The disparity has persisted, even worsened. The average household in the top 10 per cent was $274,000 richer in 2023 compared to 2019, in terms of wealth. The bottom 10 per cent was up $3,800.

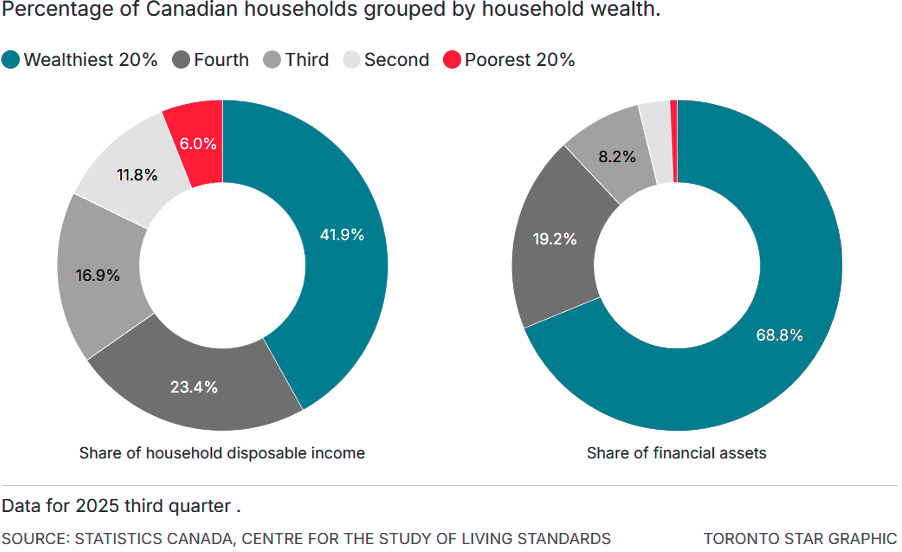

That the wealthier have more than the poor is obvious. The issue since the mid-2020s, though, is how severe the disparity is becoming. The wealth gap now is at record highs. Statistics Canada says the wealthiest 20 per cent of Canadian households hold 65.5 per cent of Canada’s total net worth as of the third quarter of 2025. The least wealthy 40 per cent hold just 3.1 per cent of wealth.

That stark gap results in some Canadians living dramatically different lives from others.

Spending power and financial assets are highly concentrated among the wealthiest 20%

Lower-income Canadians are taking on debt to get by. Before the pandemic, the debt load of an average household was about 300 per cent the size of disposable income. That has risen to 429 per cent.

If they can accumulate assets, it’s mainly their homes, not the often more liquid or profitable stocks or bonds that fuel the portfolios of the rich.

Unsurprisingly, debt-related stress has spiked. The Bank of Canada’s survey of consumer expectations shows that the number of people earning less than $40,000 who are worried they won’t be able to make their payments over the next three months has soared.

On the other hand, the debt load for the highest income group has remained fairly steady at about 130 per cent of disposable income. Their stress around being able to make payments is, as you’d expect, quite low.

Put another way, while many Canadians are increasingly worried about meeting their basic needs, the wealthy are planning fancy vacations.

Marianne, a 20-year-old member of the military who is texting her friends from a corner of a suburban Ottawa food court, wants in on that action. She joined the Forces for job security, income stability and a career path and particularly because she wanted to move out on her own and start an independent life.

She gets room and board on the nearby base, but she dreams of renting an apartment, “just to put a bit of distance between myself and work,” she says.

And so Marianne — that’s her middle name since she didn’t feel comfortable using her whole name — is saving as much of her salary as she can, and investing it in the markets with the help of her local bank branch.

She harbours no illusions of hitting the jackpot. Her holdings churn wildly. Meanwhile, apartments seem extravagantly expensive, and making monthly payments is out of her scope right now. But she has time on her side.

“It’s really a question of being patient,” she insists.

For Marianne, the key to building wealth is holding a steady job with a secure income.

Aban agrees with that. He feels the stress of unemployment, though, even though it’s only been a few months and his family is figuring out how to make ends meet.

It points to another post-pandemic K-shape. Almost half of people earning under $40,000 fear losing their job over the next 12 months, dramatically higher than before the pandemic, the global trade war and the slowdown in growth. If you’re making over $100,000, the fear is minimal.

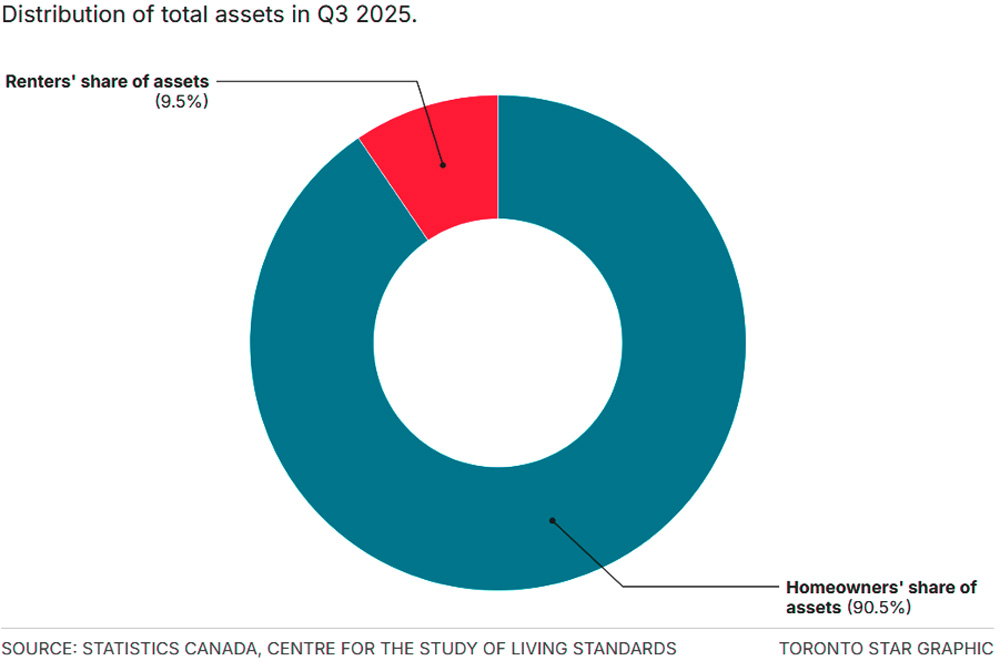

Homeownership is another key differentiator

Who, exactly, are the people who are on the anxiety-ridden front lines of low wages and the affordability crunch? They are workers in accommodation and food services, or retail. They are women. They’re often recent immigrants, and racialized Canadians — especially south Asians, Filipinos and Black Canadians. They’re living on less now than before the pandemic, since the increase in the cost of essentials has outpaced wage growth.

To be clear, this is not America. There, the economy as a whole is growing faster than Canada’s, but the job market is softer than Canada’s. Low-income American consumers are not as sturdy as they are in Canada. And while both countries have K-shaped patterns in wealth, Canada’s distribution of income — which is not the same as wealth — is less stark.

The American disparities prompt frequent warnings of things falling apart — anger, division, social unrest. We can see the destructive results of worsening inequality appearing before our eyes.

Peter Atwater, the American economist who has popularized the term “K-shaped recovery,” is now warning that inequality in the United States is creating a “caste system” that is unsustainable. There, deepening inequality is frequently linked to political polarization, the erosion of trust in institutions and the crumbling of democracy itself.

We aren’t them. But it’s a lesson on what is at risk. A progressive income-tax system, coupled with a solid social safety net, has stood Canada in good stead, softening the sharp edges off the K-shape on our side of the border.

Increasingly, however, the momentum is shifting toward those on the upper arm of the K through wealth, amassed through investment in financial markets and real estate.

It’s a situation made worse by the fact that wealth begets wealth; investment properties and stocks can compound in growth, and over years and decades, can grow exponentially.

Our progressive tax system, however, is designed to target income.

That’s a big difference, especially these days.

Income is the flow of money coming into a household, through salary, rent or interest. Wealth (or net worth), on the other hand, is the pile of assets a household owns, minus outstanding debt.

The 20 per cent of the least wealthy among us holds just 1.5 per cent of the assets in Canada’s economy, and just 0.7 per cent of the financial assets (stocks and bonds). In a world where affordability and progress — that is, the ability of households to build a nest egg and invest in new ideas — stem from the appreciation of those very assets, that’s a very thin base indeed.

The top 20 per cent, on the other hand, holds 68.8 per cent of the economy’s financial assets like stocks and bonds, and 60.1 per cent of all assets. This too has knock-on effects; assets can grow or produce income which further exacerbates the disparity in both wealth and lifestyle, too.

While the K-shaped nature of wealth accumulation and economic growth runs deep, it’s not at all static. The profound changes gushing through our country — driven by trade wars, artificial intelligence and geopolitical upheaval — mean that the low-key envy and anxiety of Canada today could easily become the resentment-fueled disruption of tomorrow.

Given the risks, it’s time for some tough questions.

Wealth divides us but our economic policy is built on our understanding of income. We need to get a better grip on how wealth grows, who owns it, where it’s stored and where it’s hidden.

And we may need to rethink how our tax policy treats those assets. Even as we keep an eye on how to invest and bolster the Canadian economy, we also need some steely-eyed scrutiny of a system that can favour those with wealth and income-generating assets — low capital-gains inclusion rates and exemptions among them, not to mention a system that is riddled with loopholes and special circumstances.

And the potentially toxic social effects of such a disparity in possibility continue to fester.

For now, we are more often resilient than rebellious.

Marianne, for one, is confident that there is a range of financial solutions available to her as she sets about building a life of independence. She has time on her side as she watches her portfolio grow in fits and starts, and she is watching the rental market closely for a chance to jump in.

Abdallah Aban’s optimism comes from context. His job hunt may have been fruitless up until now and he fears employers find him too old to bring onto their payrolls. But compared to his previous life, Canada gives him hope. He fled a civil war in Somalia to come to Canada.

“Anything is better than that,” he says. “I mostly want peace.”

Related reading

Canada’s K-shaped economy, by the numbers

What the numbers say about wealth, inequality and affordability since the pandemic. Some number-crunching by the Canadian Tax Observatory and the Centre for the Study of Living Standards.

The CRA is still playing hardball over CERB payments — while larger tax questions go unanswered

Six years ago today (March 21, 2026), the federal government closed the border to non-essential travel with the United States to curb the spread of COVID-19. They had already shut down large sections of the economy, and started issuing hundreds of millions of dollars in funding to help companies and workers deal with the pandemic.

Tax filing was supposed to be getting easier. That’s still a work in progress.

It’s tax-filing season again, with all the headaches that brings for Canadians tearing apart their houses and their laptops to find the right paperwork before the deadline.

Get in Touch

Have feedback on the work we are doing? Interested in collaborating? We want to hear from you.