What history tells us about tax, trouble and the top one per cent

By Shirley Tillotson, Professor of history at Dalhousie University; expert advisor at the Canadian Tax Observatory | A version of this piece was originally published in the Halifax Examiner, February 25, 2026

Mark Carney wasn’t the only one making a splash in Davos. So were some 400 of the world’s millionaires and billionaires.

They were out in full force asking for governments to tax them more.

They know that governments everywhere need more revenue. Especially here in Canada where the turning-away-from-the-U.S. project set out by Prime Minister Carney will require billions in government spending on defence, infrastructure, and social supports.

Perhaps a tax on billionaire wealth (a simple one-off?) would be a good source of some of that money.

But the best tool at our disposal to raise this much-needed revenue is one we are set up already to use: income tax.

“But the income tax is a mess!” you say. Too complex and yet too ineffective at reaching high incomes. Worse, it scarcely touches wealth.

Yes. And yet. Let’s revisit the origins of the federal income taxes in North America. It’s a thought-provoking story of how an old tax, one crippled by many years of evasion, led to a fairer tax system.

The old tax was the municipal property tax. In many North American cities, including Toronto, Ottawa, and others in Ontario, property tax had become hopelessly corrupted.

Individual assessors took bribes, but worse, the municipalities attempted and increasingly failed to tax “personalty” – movable assets like jewellery, carriages, boats, and “intangible” assets, such as stocks and bonds.

The full scope of taxable personalty just wasn’t visible with the assessment tools of the day. So municipalities depended on the more easily “seen” homes and goods of the non-investing classes.

Federally, too, the poor, the farmer, and the modest earner paid a disproportionate share of their incomes on customs and excise taxation, the main source of national revenue.

From the 1880s onward, tax protesters clamoured and revolts brewed.

National and international grassroots movements called for taxation of inheritances and of land. Wealth, that is.

Worse, from most millionaires’ perspective, actual socialism was gaining electoral ground.

Public ownership! Confiscation! These were real possibilities.

In Canada, fabulously wealthy financier Isaak Walton Killam deplored how slow the feds were to adopt a war income tax. Finally, the one adopted in 1917 was modeled on the 1904 Ontario municipal income tax.

In this context, a well-ordered, mildly progressive-rate tax on upper incomes was, comparatively speaking, not a terrible threat.

By the 1910s, income tax on a national scale was looking like an easy way to spike the socialists’ guns, appease the fretful farmers, and soothe the tariff-oppressed consumer.

Its advocates, both rich and poor, could point to just such a tax that was working well in Ontario. A municipal income tax, on the books since 1866, was resuscitated in 1904, slightly revised, and used to correct for the inequity of the old property tax.

Income tax became a popular proposal for national tax reform, even among the very rich. The leading advocate, economist E.R.A. Seligman, came from a family of millionaire New York bankers.

In Canada, fabulously wealthy financier Isaak Walton Killam deplored how slow the feds were to adopt a war income tax. Finally, the one adopted in 1917 was modeled on the 1904 Ontario municipal income tax.

In the postwar debate, Killam was among those who insisted that the war income tax be continued.

Looking ahead to years of interest payments on the huge war debt, parliament agreed. They decided not to impose wealth taxes (a capital levy or a land value tax), but to keep the war income tax.

As MP William Foster Cockshutt, a millionaire industrialist, said in the House in 1919, he was willing, as all Canadians must be, “to submit to heavy taxation for some years to come.”

Like Seligman, both Cockshutt and Killam knew that, without direct taxation of substantial incomes, the nation’s tax structure was discredited, as the municipalities’ had been.

In 1919, with the recent revolution in Russia and labour revolts in Winnipeg and around the world, a nod to fairness, however modest, was in the interest of security of wealth.

It was not time to reform the polarizing, unreliable tariff. It was the time to do something that had proved feasible in Ontario: tax upper incomes.

Similarly, it is not time now to thoroughly reform our income tax system. It’s time to use familiar tools to do a few straightforward things, things that are widely seen as fair.

Raise the taxable percentage of capital gains. (Yes, try again.) Eliminate tax provisions that disproportionately benefit the top 1%. (Yes, try again.)

Do something. Or wait for the equivalent of 1919.

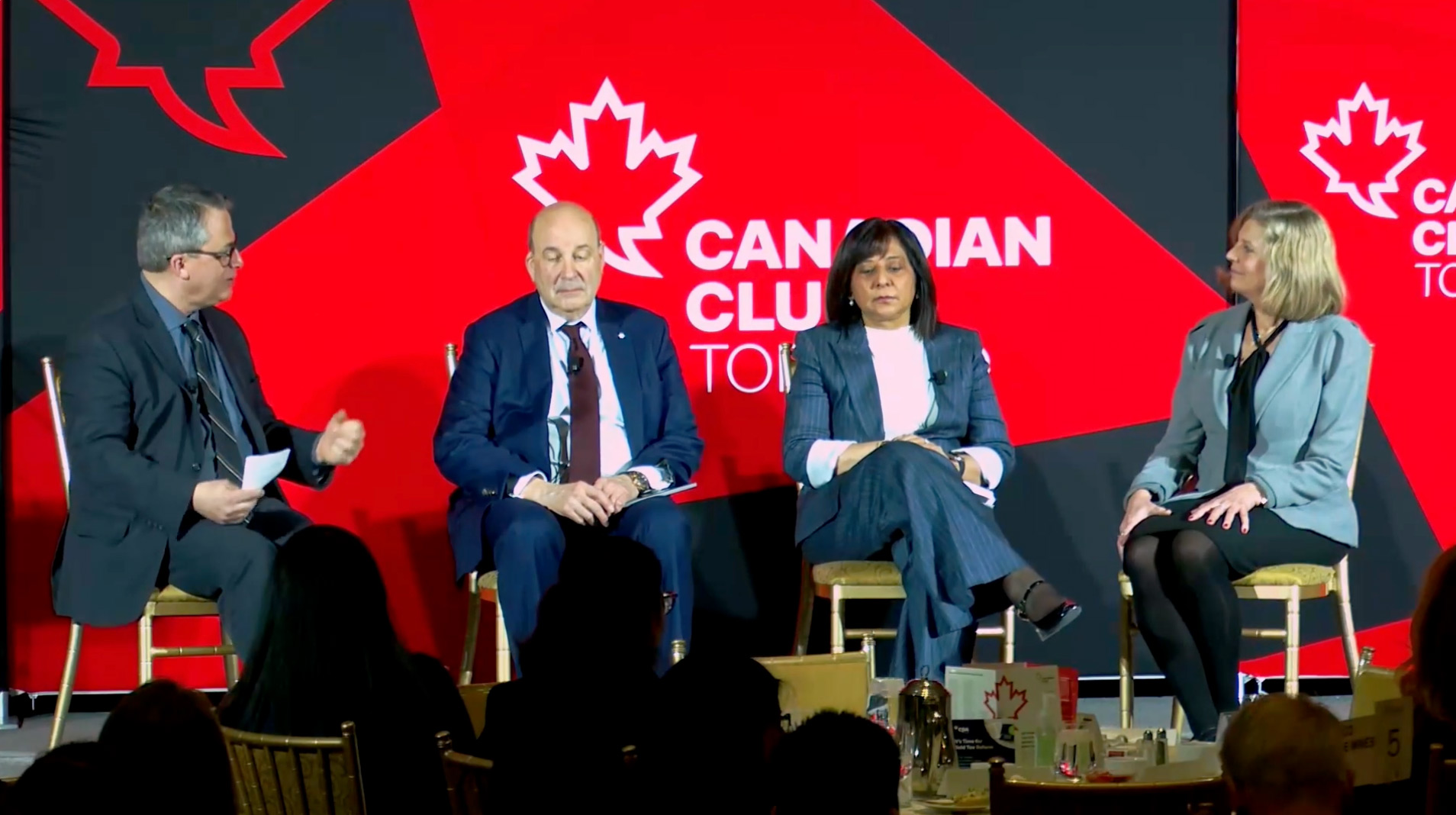

Rethinking Canada’s Tax System: What Works, What Doesn’t, What’s Next

Heather Scoffield | The Canadian Club of Toronto | February 24, 2026

The Canadian Club of Toronto hosted a panel on rethinking Canada’s tax system (what works, what doesn’t, what’s next), featuring the Canadian Tax Observatory’s Heather Scoffield, Deloitte’s Fatima Laher and the University of Calgary’s Jack Mintz. Moderated by Patrick Brethour of the Globe and Mail. Here’s a recording.

The Canadian Tax Observatory applauds new tax measures to make life more affordable

The Canadian Tax Observatory welcomes today’s announcement from Prime Minister Mark Carney and Finance Minister François-Philippe Champagne to substantially increase the GST credit, now called the Canada Groceries and Essentials Benefit.

In boosting support for low-income Canadians through the tax system, they are ensuring funds reach the hands of those who need it most — quickly, and also over the longer term.

“The prime minister’s recognition that his investment-oriented budget won’t deliver immediate returns for struggling Canadians is important,” says Heather Scoffield, the Observatory’s CEO. “A key element of Canada standing on its own in today’s turbulent economy is ensuring regular people are able to make ends meet.”

About the Canadian Tax Observatory

Established in 2025, the Canadian Tax Observatory is an independent non-profit devoted to helping people and policymakers understand the tax system. Through research, public education and collaboration, its goal is to advance a tax system that promotes economic growth, shared prosperity and tax fairness. It aims to drive an informed public dialogue in pursuit of practical taxation that benefits all Canadians. Through solid, independent research and non-partisan public engagement, we encourage fresh thinking that leads to practical solutions on tax policy. The founding CEO is Heather Scoffield, whose expertise lies in informing and driving national conversations on economic policy.

For more information, please contact:

Heather Scoffield

CEO

heather@canadiantaxobservatory.ca

613-314-1198

Find me on LinkedIn | X | Substack

Global minimum tax, and America’s message to the world: Trust us — as if

By Heather Scoffield | Originally written for the Toronto Star on January 17, 2026

From a distance, it looks like a dirty trick.

The United States leads the world into a negotiation for a global minimum tax. Eventually, painfully, everyone agrees to a complicated, finely-balanced pact that would ensure big multinational corporations all pay at least 15 per cent in taxes.

The goal is a global level playing field and an end to the tax-slashing race to the bottom to attract business.

At the last moment, the U.S. demands and is granted exemptions for its own — the biggest, most powerful companies in the world. And 147 other countries are left wondering whether the pact they’re signing is worth the paper it’s written on.

But sign, they do — mainly to salvage what they can from years of arcane wordsmithing in the hopes of preserving their own tax bases and sidelining global tax havens.

It’s come to this.

In a Donald Trump world where the U.S. routinely bails from international agreements, ignores longstanding rules of engagement and storms ahead in its own interests oblivious of the consequences, convincing Canada and other supporters of the global minimum tax to allow an America-friendly side-agreement seems almost quaint.

But it’s serious business that implicates Canada’s scope to preserve its tax base, compete and share the proceeds.

The global minimum tax talks actually started out on a note of optimism and American leadership.

While many countries had long decried multinational companies’ crafty use of the low- or no-tax rates in some jurisdictions, the campaign to end tax avoidance took a major leap forward in 2021 when then-U.S. Treasury Secretary Janet Yellen threw her considerable influence behind gritty discussions at the Organization for Economic Cooperation and Development.

Canada’s then-finance minister Chrystia Freeland was a close ally, agreeing wholeheartedly with Yellen that a worldwide floor for corporate tax would stymie a global race to the bottom, allow Canada to maintain its corporate tax base and benefit workers with a fairer tax system.

But Canada also hedged its bets, just in case the complex OECD talks didn’t work out. Freeland announced a parallel Digital Services Tax to target large, multinational digital companies active in Canada. As the global talks stumbled, Canada enacted the DST in 2024, making it retroactive to 2022.

As we know, that plan never materialized — going toe-to-toe with Trump’s agenda and losing. And it’s that altercation which can explain the compromises that led to today’s arrangement.

The key moment was last June, just as the DST was about to take effect.

Trump showed up at the G7 summit in Kananaskis, Alta., armed with the dreaded Section 899 of the One Beautiful Bill Act — also known as the “revenge tax.” Countries that embraced the global minimum tax agreement, and especially those who adopted their own DSTs, would face retaliatory high tax rates on individuals making money in the United States.

Under intense pressure from their business communities, the G7 stood down, Canada nixed its DST, and the G7 instead offered up a special arrangement for American companies. Trump removed the revenge tax provision, and the U.S. returned to the global minimum tax table.

And here we are, telling ourselves we’re lucky that the U.S. agreed to anything at all.

The so-called side-by-side agreement announced this month is designed to recognize U.S. arguments that its corporate tax system is fine as it is since it already mirrors what everyone else has signed on to in the main agreement. It doesn’t recognize the U.S. by name, but they’re the only ones who qualify.

The so-called side-by-side agreement announced this month is designed to recognize U.S. arguments that its corporate tax system is fine as it is since it already mirrors what everyone else has signed on to in the main agreement. It doesn’t recognize the U.S. by name, but they’re the only ones who qualify.

Treasury Secretary Scott Bessent hailed it as “a historic victory in preserving U.S. sovereignty and protecting American workers and businesses from extraterritorial overreach.”

It may be a side quest for the U.S., but there are significant implications for the rest of the world — especially since the severe disruption in the global economy means Canada and many other countries are parched for investment and are actively redesigning their investment incentives to be more aggressive.

To be sure, the new package gives Canada some stability as it goes about the hunt for private-sector dollars. And perhaps, if the overall agreement works as intended, tax haven countries will rein in their competitive tax-slashing.

But the side deal gives leeway to the U.S. to decide for itself, at least in some instances, what counts and what doesn’t in the calculation of tax. And it leaves Big Tech and other American corporations alone to continue as they have been, booking up to half their foreign profits in tax havens, according to the EU Tax Observatory.

Meanwhile, the overall deal that Canada is signing on to means tax is no longer much of a tool to attract investment. We do have other, more effective tools — subsidies, predictability, rule of law, and industrial policy writ large. It could be a lot worse.

But it’s not clear the Americans will constrain themselves accordingly. The understood message from America is: trust us.

As if.

The Canadian Tax Observatory welcomes powerhouse advisory committee of experts

Today, the Canadian Tax Observatory announced the nine prominent tax thinkers who will form its founding expert advisory committee.

“I’m looking forward to working with this impressive group to guide the Observatory’s ambitious strategy and research agenda to advance fair taxation in Canada,” says CEO Heather Scoffield. “Taxation issues are complex and multilayered. This team reflects that, with deep expertise across academia, policymaking, tax law, accounting, economics and investment.”

The committee will meet twice a year and provide frequent consultation to guide the Observatory’s expert analysis and public engagement. Drawing on their diverse perspectives and experience, they will inform a rigorous and sophisticated approach to understanding the real-world implications of tax policy on Canadians’ economic lives.

L’Observatoire canadien de la fiscalité a dévoilé aujourd’hui les noms des neuf éminents spécialistes de la fiscalité qui composeront son nouveau comité d’experts.

« Je me réjouis à la perspective de travailler avec un groupe d’une telle envergure, qui accompagnera l’Observatoire dans ses ambitions et contribuera à orienter sa stratégie et ses travaux de recherche en faveur de l’équité fiscale au Canada », indique la cheffe de la direction, Heather Scoffield. « Les enjeux liés à la fiscalité sont complexes et pluridimensionnels. La composition de cette équipe en est l’illustration, puisqu’elle rassemble de grands spécialistes issus du monde universitaire et des domaines des politiques publiques, du droit fiscal, de la comptabilité, de l’économie et des placements. »

Le comité se réunira deux fois par an et conseillera fréquemment l’Observatoire dans ses analyses spécialisées et ses interventions auprès du public. La diversité des points de vue et des expériences de ses membres nourrira une réflexion rigoureuse et éclairée sur l’impact de la politique fiscale sur la vie économique des Canadiens.

Advisory Committee Members

David Duff

Professor of Law and Director of the Tax LLM program at the Peter A. Allard School of Law at the University of British Columbia.

Antoine Genest-Gregoire

Assistant Professor of the Department of Taxation at the University of Sherbrooke and a researcher under its Research Chair in Taxation and Public Finance

Anish Makim

Partner at ExCap Advisors and a senior business advisor in Canada’s telecommunications sector

Kevin Milligan

Professor and Director of the Vancouver School of Economics at the University of British Columbia and Research Associate of the National Bureau of Economic Research

Carman McNary

Tax and corporate lawyer at Dentons Canada LLP, providing strategic advice to companies and their boards, First Nations and FN business groups, non-profit and charitable organizations

Elena Patel

Co-Director of the Urban-Brookings Tax Policy Center, the Pozen Director’s Chair, and a Senior Fellow in Economic Studies at the Brookings Institution

Sandra Rosier

Tax advisor and, lawyer; and Founder and principal at Rosier Tax Advisory, which provides tax counsel to pension funds, global asset managers and financial institutions

Charles St-Arnaud

Chief Economist at Servus Credit Union

Shirley Tillotson

Professor of History at Dalhousie University and author of award-winning Give and Take: The Citizen-Taxpayer and the Rise of Canadian Democracy

For more information, contact:

Heather Scoffield, CEO

The Canadian Tax Observatory

heather@canadiantaxobservatory.ca

Cell: 613-314-1198

Shirley Tillotson

universedev1

Dr. Shirley Tillotson is Professor of History at Dalhousie University. She was the 2019 recipient of the Governor General’s History Award for Scholarly Research for her book, Give and Take: The Citizen-Taxpayer and the Rise of Canadian Democracy. This, and her other work on Canadian tax history, are part of her general research interest as a historian in the tissue of connections between the institutions of government and the relationships of daily life and civil society. In addition to continuing scholarly research, she has, since her retirement from the classroom, brought a Canadian historical perspective to journalism and social media conversations.

Charles St-Arnaud

universedev1

Charles St-Arnaud is Chief Economist at Servus Credit Union. He has more than 20 years of experience as an economist in the public and private sector, both in Canada and internationally. Before joining Servus, he was Chief Economist at Alberta Central. Before that, Charles focused on global financial markets as Senior Investment Strategist at Lombard Odier Investment Manager in London, England, and as Senior Economist and FX Strategist at Nomura International in New York City and London.

Charles was at the Department of Finance in Ottawa during the global financial crisis, where he advised senior officials. He also worked for the Bank of Canada and Morgan Stanley. He is a regular contributor to the Financial Post, The Globe andMail, BNN Bloomberg, CBC/Radio-Canada and the Calgary Herald. Charles holds an MSc in Economics from the Université du Québec à Montréal.

Sandra Rosier

universedev1

Sandra Rosier is a tax advisor, lawyer and Founder and Principal at Rosier Tax Advisory, which provides tax counsel to pension funds, global asset managers and financial institutions. Prior to starting her own practice, Sandra was Global Head of Tax at BGO, where she oversaw the tax function. Previously, she was Managing Director of Tax in the finance group at CPP Investments. Sandra started her career in private practice at McCarthy Tétrault LLP and Ropes & Gray LLP. She holds a J.D. from the University of Ottawa and is a member of the Law Society of Ontario and the Massachusetts Bar.

Elena Patel

universedev1

Elena Patel is Co-Director of the Urban-Brookings Tax Policy Center, the Pozen Director’s Chair and a Senior Fellow in Economic Studies at the Brookings Institution. Her research examines how tax systems, health programs and social safety nets shape economic behaviour and well-being. She studies how tax policy affects investment and capital accumulation, how incentives and risks influence employment decisions and how governance and health policy intersect with labour markets and economic security.

Elena also serves as a Fiscal Policy Impact Scholar at the University of Utah’s Marriner S. Eccles Institute. Previously, she was the Sorenson Assistant Professor at the University of Utah’s David Eccles School of Business and held several federal government positions, including serving as Senior Public Finance Economist at the White House Council of Economic Advisers and as an economist at the U.S. Treasury. She holds a Ph.D. in Economics from the University of Michigan.

Kevin Milligan

universedev1

Kevin Milligan is Professor and Director of the Vancouver School of Economics at the University of British Columbia and Research Associate of the National Bureau of Economic Research. Since 2011, he has served as Co-Editor of the Canadian Tax Journal. He studied at Queen’s University and the University of Toronto, receiving his Ph.D. in 2001. His published research in over 100 articles spans the fields of public and labour economics, with a primary focus on how the Canadian tax and transfer system affects economic decisions and well-being. In 2020-21, he served as Special Advisor (Economic Recovery) in Canada’s Privy Council Office.