Broken Links: Poverty and the Limits of the Disability Tax Credit — Snapshot by Canadian Tax Observatory CEO Heather Scoffield

By Heather Scoffield

Prime Minister Mark Carney was passionate when he addressed party members in Montreal in early April, eloquent in his appeal to Canadians’ universal values as a primary defence against global strife.

“We believe in a just society where we take care of the vulnerable, where we pull together to make life more affordable today and better tomorrow,” he said.

He went on to say that his government is recommitting to that mission, “to build a Canada that’s not just strong, but good; a Canada that’s not just prosperous but fair; a Canada not just for some most of the time, but for all—all of the time.”

That close correlation between fair economic policy and deep social cohesion is central to his statements, and it’s also central to this report.

But we have a serious problem.

More than a quarter of Canada’s working age population has a disability of some kind – about eight million Canadians—and the numbers are rising as the population ages. Where the serious and stubborn problem lies is in the fact that poverty among people with disabilities is pervasive—despite multiple layers of government programs and supports.

The poverty rate among people with disabilities is double that of their non-disabled peers, and after a slight improvement before 2020, that rate has since deteriorated.

The hope was that this would change with the Canada Disability Benefit, enacted in 2023 and implemented in July 2025. But there’s a catch. To get that benefit and at least 12 other income-related supports, a person must first be certified for the Disability Tax Credit (DTC).

“That design choice places the DTC—a non-refundable tax credit created for tax equity purposes, not income support—at the centre of Canada’s disability poverty reduction architecture,” writes University of Calgary researcher Gillian Petit.

And that’s a barrier to 84 per cent of people with disabilities. Only 16 per cent of that population has qualified for the DTC and the access that certification brings to other, crucial programs.

Her report for the Canadian Tax Observatory identifies four different links in the system that a person with a disability must steer through to access proper income security and support: eligibility, certification, access to other programs that require DTC certification, and benefit adequacy.

Petit’s four-link framework for analysis provides a clear and practical way to understand where the system breaks down. Her framework opens the door to pragmatic, near-term solutions for a system that is convoluted, costly for applicants and administrators alike, and difficult to navigate for many—especially those without resources.

Each link has serious flaws that deter or prevent hundreds of thousands of people from accessing benefits.

- Eligibility: The DTC defines disability as a severe and prolonged impairment that restricts basic activities for 90 per cent of the time for 12 months in a row. That definition can exclude many individuals with episodic, mental health and pain-related disabilities.

- Certification: Deterrents to obtaining the DTC certificate include a 16-page application, the time and cost of engaging a qualified medical practitioner to give a stamp of approval, and an opaque adjudication process.

- The DTC as a gateway to other programs: At least 12 programs require applicants to hold a DTC certificate. But even with a certificate in hand, applicants face additional requirements such as tax filing.

- Benefit Adequacy: Even if applicants manage to navigate through the links in the DTC system and finally qualify for the Canada Disability Benefit, it amounts to a maximum of $2,400 a year – a modest amount that, on its own, is insufficient to lift most people out of poverty.

It’s possible to strengthen the system by addressing the weak links in the chain, step by step. This report is meant to provide a structured framework to identify where fixes in the DTC system are most likely to improve outcomes for people with disabilities.

It touches on legislative change that could expand the eligibility criteria for the DTC. It proposes administrative reforms to improve access to the certification process.

And it sets out a series of research priorities to better understand how a well-supported, more simplified and more automated system of certification would work for low-income people with disabilities.

What it does not do is examine in detail the adequacy of benefits that are interconnected, which has been examined elsewhere and is beyond the scope of this paper.

Rather, the report focuses on what’s before us right now: the structure of the Disability Tax Credit, the benefits it unlocks and the broken links in the system. It’s a detailed invitation to government officials, advocates and other researchers to put those universal Canadian values into practice and figure out how to repair a faulty system that stands in the way of that prosperous, fair country we aim for.

Les failles d’un système : pauvreté et limites du crédit d’impôt pour personnes handicapées — Aperçu par la cheffe de la direction de l’Observatoire canadien de la fiscalité, Heather Scoffield

Début avril, le premier ministre Mark Carney a livré un discours passionné devant les membres de son parti réunis à Montréal : les valeurs canadiennes, a-t-il plaidé, constituent un rempart essentiel contre les tensions mondiales.

« Nous croyons en une société juste, où l’on prend soin des plus vulnérables et où l’on travaille tous ensemble pour rendre la vie plus abordable aujourd’hui et meilleure demain », a-t-il déclaré.

Il a ajouté que son gouvernement se redonnait la mission « de bâtir un Canada qui ne soit pas seulement fort, mais bon; un Canada qui ne soit pas seulement prospère, mais juste; un Canada qui ne soit pas seulement là pour quelques-uns la plupart du temps, mais là pour tous, tout le temps ».

Ce lien étroit entre l’équité des politiques économiques et la cohésion sociale occupe une place centrale dans ses déclarations et est également au cœur de ce rapport.

Il y a toutefois un gros problème.

Plus du quart de la population canadienne en âge de travailler, soit environ 8 millions de personnes, vit avec une forme ou une autre de handicap et ce chiffre continue d’augmenter avec le vieillissement de la population. Ce qui est particulièrement préoccupant, c’est que la pauvreté est répandue chez les personnes en situation de handicap, malgré toutes les aides et les programmes publics.

Le taux de pauvreté chez les personnes en situation de handicap est deux fois plus élevé que chez les personnes sans handicap, et, après une légère amélioration avant 2020, il a recommencé à augmenter.

On espérait que les choses changeraient avec l’adoption, en 2023, de la Prestation canadienne pour les personnes handicapées et sa mise en œuvre en juillet 2025. Mais il y a un hic. Pour bénéficier de cette prestation et d’au moins 12 autres mesures de soutien liées au revenu, il faut d’abord être reconnu admissible au crédit d’impôt pour personnes handicapées (CIPH).

« Ce choix place le CIPH – un crédit d’impôt non remboursable conçu pour des raisons d’équité fiscale, et non comme mesure de soutien du revenu – au cœur du dispositif canadien de lutte contre la pauvreté chez les personnes en situation de handicap », souligne Gillian Petit, de l’Université de Calgary.

Et il constitue un obstacle pour 84 % des personnes en situation de handicap. À peine 16 % d’entre elles ont été reconnues admissibles au CIPH et peuvent, de ce fait, accéder aux autres programmes essentiels qui en dépendent.

Dans un rapport préparé pour l’Observatoire canadien de la fiscalité, Gillian Petit met en évidence les quatre maillons du système de soutien au revenu auxquels se heurtent les personnes en situation de handicap : l’admissibilité, la certification, l’accès aux autres programmes conditionnels au CIPH et l’adéquation des prestations.

Ce cadre d’analyse en quatre points permet de repérer clairement les lacunes du système. Il ouvre la voie à des solutions pratiques à court terme pour remédier à un système à la fois complexe, coûteux pour les demandeurs comme pour les administrations, et difficile à comprendre pour bien des gens, surtout pour ceux qui manquent de ressources.

Chacun de ces maillons comporte de sérieuses lacunes qui dissuadent ou empêchent des centaines de milliers de personnes d’accéder aux prestations.

- Admissibilité : Pour être admissible au CIPH, il faut présenter une déficience grave et prolongée qui restreint les activités de base 90 % du temps sur une période de 12 mois consécutifs. Cette définition exclut de nombreuses personnes présentant des incapacités épisodiques, des troubles de santé mentale ou des limitations liées à la douleur.

- Certification : Pour être reconnu admissible au CIPH, il faut remplir une demande de 16 pages, la faire approuver par un professionnel de la santé qualifié, ce qui prend du temps et de l’argent, et se soumettre à un processus d’évaluation opaque.

- Accès aux autres programmes : Pas moins de 13 programmes distincts dépendent de l’obtention du CIPH. Même une fois cette condition remplie, d’autres exigences peuvent s’appliquer, comme la production d’une déclaration de revenus.

- Adéquation des prestations : Quand bien même les demandeurs franchiraient tous les obstacles et accéderaient à la Prestation canadienne pour les personnes handicapées, celle-ci est plafonnée à 2 400 $ par an et demeure, à elle seule, insuffisante pour sortir la plupart des personnes concernées de la pauvreté.

On peut renforcer le système en s’attaquant, une par une, à chacune de ses failles. Le présent rapport propose un cadre structuré pour déterminer où des correctifs au régime du CIPH sont les plus susceptibles d’améliorer les choses pour les personnes en situation de handicap.

Il se penche sur certaines pistes de réforme législative qui pourraient permettre d’élargir les critères d’admissibilité au CIPH. Il propose des changements administratifs pour améliorer l’accès au processus de certification.

Il présente également une série de priorités de recherche visant à mieux comprendre en quoi un système de certification mieux encadré, plus simple et davantage automatisé pourrait améliorer les choses pour les personnes en situation de handicap à faible revenu.

En revanche, le rapport n’aborde pas en détail l’adéquation des prestations interconnectées, le sujet ayant déjà été traité ailleurs et dépassant le cadre de cette analyse.

Il s’attarde plutôt aux enjeux immédiats : la structure du crédit d’impôt pour personnes handicapées, les prestations auxquelles il donne accès et les failles du système. Il invite concrètement les décideurs publics, les défenseurs des droits des personnes handicapées et les autres chercheurs à mettre ces valeurs canadiennes en pratique et à trouver comment remédier aux failles d’un système qui freine l’avènement d’une société prospère et équitable.

See the report

Broken Links

Only 16 per cent of people with disabilities qualify for the Disability Tax Credit and the access that certification brings to other, crucial programs. New research from Dr. Gillian Petit identifies four different links in the system that a person with a disability must steer through to access proper income security and support.

Broken Links

Poverty and the limits of the Disability Tax Credit

The Disability Tax Credit (DTC) was initially set up to account for higher day-to-day costs faced by people with disabilities. In 2023, however, the federal government introduced the Canada Disability Benefit and required certification for the DTC as a prerequisite, turning the DTC into a “gateway” for programs and policies that can make or break a person’s ability to make ends meet.

New research from the Canadian Tax Observatory authored by Dr. Gillian Petit finds that 84 per cent of people with disabilities do not have DTC certification—and can’t access the other disability programs it is intended to unlock. This means the majority of people who could benefit for federal disability supports are excluded before they can access them.

The report examines and dissects the tangled web of process and bureaucracy connected to the DTC and finds that at every step along the way, there are deep flaws and barriers that perpetuate the very poverty trap it is meant to alleviate.

Canada's Disability Tax Credit stymies 84% of those it’s meant to help

Almost everyone in Canada knows a person with a disability. At last count, more than a quarter of the population over the age of 15—about eight million people—had either a physical or mental disability.

Here’s a disturbing fact: a disproportionate share of this population lives below the poverty line—roughly double the rate of those without disabilities.

And here’s another disturbing fact: An overwhelming majority are not accessing the income supports available to them due to a system that is complex, costly and difficult to navigate.

This according to a new report released today by the Canadian Tax Observatory and authored by University of Calgary researcher Gillian Petit, taking a detailed look at the Disability Tax Credit (DTC) and its role in channeling support for those who need it most.

They find that the DTC is a chain of broken links that limits access to support.

The DTC was initially set up to account for higher day-to-day costs faced by people with disabilities, and wasn’t meant to be an anti-poverty measure per se. In 2023, however, the federal government introduced the Canada Disability Benefit and required certification for the DTC as a prerequisite. Since then, 13 government support systems have been tied to DTC certification, turning the DTC into a “gateway” for programs and policies that can make or break a person’s ability to make ends meet.

In fact, the term “gateway” is too generous.

About 84 per cent of people with disabilities do not have DTC certification and can’t access the other disability programs it is intended to unlock. This means the majority of people who could benefit for federal disability supports are excluded before they can access them.

The report examines and dissects the tangled web of process and bureaucracy connected to the DTC and finds that at every step along the way, there are deep flaws and barriers that perpetuate the very poverty trap it is meant to alleviate.

“The majority of persons with disabilities who are potentially eligible for the Disability Tax Credit (DTC) do not hold a DTC certificate,” Petit writes in the study, Broken Links: Poverty and the limits of the Disability Tax Credit.

“The gaps in certification are not random: they fall disproportionately on women, persons with mental health and episodic disabilities and those in the lowest income quintile—the groups for whom the gateway programs the Disability Tax Credit unlocks are most consequential.”

The flaws are embedded throughout the system surrounding the DTC.

Eligibility is narrow, confined by a definition of disability that bears little resemblance to real life.

The certification process is complex and often costly, requiring medical documents, finding medical practitioners to vouch for them and repeated administrative steps.

And even once those barriers are cleared, each program attached to the DTC comes with additional bureaucracy, eligibility criteria and further administrative steps.

Improvements are possible and necessary if Canada is serious about building a resilient economy and reducing poverty among persons with disabilities. In the short term, administrative and legislative changes could help with access and cost, Petit shows. However, the report suggests that broader reform of the DTC and the system it supports are required.

The federal government has indicated it is open to reviewing the DTC—a welcome start, but not just nice to have. The Canadian Tax Observatory will undertake more research to propose practical solutions to a problem that has persisted for decades.

About Gillian Petit

Gillian conducts research focused on intersectionality informed, data-driven solutions to economic and social issues in Canada. Her work in economics and public policy focuses on the design and implementation of income and social supports spanning several areas including tax policy, municipal policy, poverty policy and access to justice. She has advised expert panels, including the B.C. Basic Income Panel, published in peer-reviewed academic journals and has co-written a book on basic income. She works as a Senior Research Associate at the University of Calgary, leading and conducting research on how government programs support economic inclusion. Gillian holds a PhD in Economics from the University of Calgary and a Juris Doctorate from Queen’s University.

For more information, or to arrange an interview with Gillian (English) or Heather (English and French), please contact:

Heather Scoffield, CEO

The Canadian Tax Observatory

heather@canadiantaxobservatory.ca

Cell: 613-314-1198

Le crédit d’impôt pour personnes handicapées du Canada laisse de côté 84 % des personnes qu’il est censé aider

Au Canada, à peu près tout le monde ou presque connaît quelqu’un en situation de handicap. Selon les données les plus récentes, plus du quart des Canadiens de plus de 15 ans, soit environ 8 millions de gens, vivent avec une incapacité physique ou mentale.

Fait préoccupant : ces personnes sont proportionnellement plus nombreuses à vivre sous le seuil de pauvreté – le taux est à peu près deux fois plus élevé que chez les personnes sans incapacité.

Autre élément tout aussi préoccupant : la plupart ne reçoivent pas les aides au revenu auxquelles elles ont droit, en raison d’un système complexe, coûteux et difficile d’accès.

C’est ce qui ressort d’un nouveau rapport publié aujourd’hui par l’Observatoire canadien de la fiscalité et rédigé par la chercheuse de l’Université de Calgary Gillian Petit, qui examine en détail le crédit d’impôt pour personnes handicapées (CIPH) et sa capacité à acheminer l’aide à celles et ceux qui en ont le plus besoin.

Sa conclusion : le processus menant au CIPH comporte de nombreux points faibles qui empêchent les personnes en situation de handicap de bénéficier de toute l’aide à laquelle elles ont droit.

Le CIPH a d’abord été conçu pour compenser le surcroît de dépenses engendré par le handicap, et ne constituait pas à proprement parler une mesure de lutte contre la pauvreté. En 2023, toutefois, le gouvernement fédéral a instauré la Prestation canadienne pour les personnes handicapées, et en a conditionné l’accès à l’obtention du CIPH. Aujourd’hui, 13 mesures d’aide sont liées à l’obtention du CIPH, si bien que celui-ci est devenu la « porte d’entrée » vers des programmes et des politiques qui peuvent faire une différence majeure dans la capacité des personnes concernées à joindre les deux bouts.

En réalité, parler de « porte d’entrée » est encore trop généreux.

Environ 84 % des personnes en situation de handicap n’ont pas accès au CIPH, ce qui les prive des programmes qui en découlent. Résultat : la majorité des gens qui pourraient profiter de ces mesures d’aide fédérales en sont exclus d’emblée.

Le rapport décortique l’enchevêtrement de processus et d’éléments bureaucratiques entourant le CIPH et constate, à chaque étape, de profondes lacunes et des obstacles majeurs qui perpétuent le piège de la pauvreté qu’il est pourtant censé atténuer.

« La plupart des personnes handicapées qui pourraient avoir droit au crédit d’impôt pour personnes handicapées (CIPH) n’ont pas de certificat de CIPH », écrit Gillian Petit dans le rapport, intitulé Les failles d’un système : pauvreté et limites du crédit d’impôt pour personnes handicapées, en anglais seulement.

« Ce non-accès au CIPH n’est pas le fruit du hasard : il touche proportionnellement davantage les femmes, les personnes qui présentent un trouble de santé mentale et des incapacités épisodiques et celles qui se situent dans le quintile de revenu le plus faible, soit les groupes pour lesquels les programmes d’aide auxquels le CIPH donne accès sont les plus importants. »

Les failles se situent à tous les niveaux du système entourant le CIPH.

Les critères d’admissibilité sont restrictifs, et reposent sur une définition du handicap qui n’a pas grand-chose à voir avec la réalité.

Le processus de certification est complexe et souvent coûteux : il faut présenter des documents médicaux, demander l’attestation de professionnels de la santé et multiplier les démarches administratives.

Et même une fois tous ces obstacles franchis, ce n’est pas terminé, puisque chacun des programmes liés au CIPH s’accompagne de son propre lot de formalités et de critères d’admissibilité.

Des améliorations sont possibles et nécessaires si le Canada veut réellement bâtir une économie résiliente et réduire la pauvreté parmi les personnes en situation de handicap. À court terme, des modifications administratives et législatives pourraient améliorer l’accès et réduire les coûts, montre Gillian Petit. Le rapport conclut toutefois à la nécessité d’une réforme plus vaste du CIPH et du système qui l’entoure.

Le gouvernement fédéral s’est dit ouvert à revoir le CIPH. C’est un bon début, mais on ne doit pas s’arrêter là. L’Observatoire canadien de la fiscalité poursuivra ses travaux afin de proposer des solutions concrètes à un problème qui dure depuis des décennies.

À propos de Gillian Petit

Gillian Petit mène des recherches sur des solutions aux enjeux économiques et sociaux au Canada, selon une approche intersectionnelle et fondée sur les données. Ses travaux en économie et en politiques publiques portent sur la conception et la mise en œuvre d’aides sociales et de soutiens au revenu dans plusieurs domaines, dont la politique fiscale, les politiques municipales, les politiques de lutte contre la pauvreté et l’accès à la justice. Elle a conseillé des groupes d’experts, dont le B.C. Basic Income Panel (groupe d’experts sur le revenu de base de la Colombie-Britannique), a publié des articles dans des revues scientifiques avec comité de lecture et a coécrit un ouvrage sur le revenu de base. Elle est associée de recherche principale à l’Université de Calgary, où elle dirige et mène des recherches sur la contribution des programmes publics à l’inclusion économique. Gillian Petit est titulaire d’un doctorat en économie de l’Université de Calgary et d’un Juris Doctor de l’Université Queen’s.

Pour en savoir plus ou pour une entrevue avec Gillian Petit (en anglais) ou avec Heather Scoffield (en français ou en anglais), veuillez communiquer avec :

Heather Scoffield, cheffe de la direction

L’Observatoire canadien de la fiscalité

heather@canadiantaxobservatory.ca

Cellulaire : 613 314-1198

See the report

Broken Links

Only 16 per cent of people with disabilities qualify for the Disability Tax Credit and the access that certification brings to other, crucial programs. New research from Dr. Gillian Petit identifies four different links in the system that a person with a disability must steer through to access proper income security and support.

About the Canadian Tax Observatory

Established in 2025, the Canadian Tax Observatory is an independent non-profit devoted to helping people and policymakers understand the tax system. Through research, public education and collaboration, its goal is to advance a tax system that promotes economic growth, shared prosperity and tax fairness. It aims to drive an informed public dialogue in pursuit of practical taxation that benefits all Canadians. Through solid, independent research and non-partisan public engagement, we encourage fresh thinking that leads to practical solutions on tax policy. The founding CEO is Heather Scoffield, whose expertise lies in informing and driving national conversations on economic policy.

For more information, please contact:

Heather Scoffield

CEO

heather@canadiantaxobservatory.ca

613-314-1198

Find me on LinkedIn | X | Substack

Shelter vs. Tax Shelter

A look at who benefits from tax measures in the housing sector

The Canadian Tax Observatory has some new research looking into the implications of tax incentives in the housing sector, especially the ever-popular FHSA.

Over the years, Canadians have poured more and more of their savings into residential investment. Economy-wide, the allure of real estate has acted like a magnet, potentially pulling money away from other sectors, most notably business investment.

There’s a cost, of course. It comes in the form of foregone revenue to the federal purse – money that could go towards any number of programs. It also comes in the form of exacerbating some of the more disturbing trends in our economy: intergenerational inequities and the gap between rich and poor. And in the end, by driving more demand for houses, such measures actually undermine their stated purpose, making housing less affordable over time.

Key findings:

- Exposure:

Canada allocates a large and rising share of its total investment to housing; and low- and middle-income households are particularly exposed to market dynamics. The affordability problem for younger and lower-wealth households is especially acute. - Bestowing Favour:

The First Home Savings Account is generous and popular, benefiting higher-income households and often funded by the so-called Bank of Mom and Dad. - Fiscal Cost:

Federal tables show that housing tax expenditures amount to about $17 billion in foregone revenue every year – a major and increasingly significant part of the federal tax system.

À qui profitent les mesures fiscales dans le secteur du logement?

Le compte d’épargne libre d’impôt pour l’achat d’une première propriété (CELIAPP) connaît un engouement incroyable. Lors de sa mise en place en 2023 par le gouvernement fédéral, il avait été présenté comme un programme destiné à aider les jeunes à accéder à la propriété. Toutefois, selon un nouveau rapport par l’Observatoire canadien de la fiscalité, les données brossent un portrait bien différent.

Au fil des ans, les Canadiens ont investi une part de plus en plus importante de leur épargne dans l’immobilier résidentiel. À l’échelle de l’économie, l’immobilier agit comme un aimant et détourne les capitaux d’autres secteurs, privant notamment les entreprises de certains investissements.

Il y a un coût à cela, bien entendu. Ces mesures privent notamment le Trésor fédéral de recettes qui pourraient financer toutes sortes de programmes. Elles exacerbent par ailleurs certains phénomènes plus inquiétants au sein de notre économie, à savoir les inégalités intergénérationnelles et l’écart entre riches et pauvres. Et, au bout du compte, en faisant grimper la demande de logements, ces mesures vont dans les faits à l’encontre des objectifs pour lesquels elles ont été conçues, en contribuant à la détérioration de l’abordabilité.

Principales conclusions

- Risque :

Le Canada consacre une part importante et de plus en plus élevée de son investissement total au logement; et les ménages à revenus faibles et moyens sont spécialement vulnérables aux dynamiques de marché. Le problème de l’abordabilité est particulièrement aigu pour les ménages les plus jeunes et les moins bien nantis. - Des avantages inégeaux :

Le compte d’épargne libre d’impôt pour l’achat d’une première propriété est généreux et populaire, il profite aux ménages aux revenus les plus élevés et ce sont souvent les parents qui cotisent. - Coût budgétaire:

Les données fédérales montrent que les mesures fiscales liées au logement privent le gouvernement fédéral d’environ 17 milliards de dollars de recettes chaque année et qu’elles constituent une part importante et toujours plus élevée du système fiscal fédéral.

Québec’s 2026-2027 Budget: Continuity heading into the October elections

By Antoine Genest-Gregoire, Assistant Professor at the University of Sherbrooke’s Department of Taxation. He is also a member of the Canadian Tax Observatory’s advisory committee.

Finance Minister Eric Girard presented his eighth budget on March 18th, 2026. This is the last budget that will be tabled before Quebecers go to the polls on October 5th. This is also the last budget of outgoing Premier François Legault who announced recently that he was stepping down as party leader. His replacement as leader of Coalition Avenir Québec will be elected on April 12th. Communication about this year’s budget was heavily focused on continuity and “leaving the house in order”, as Girard has often described the financial challenge he himself inherited 8 years ago.

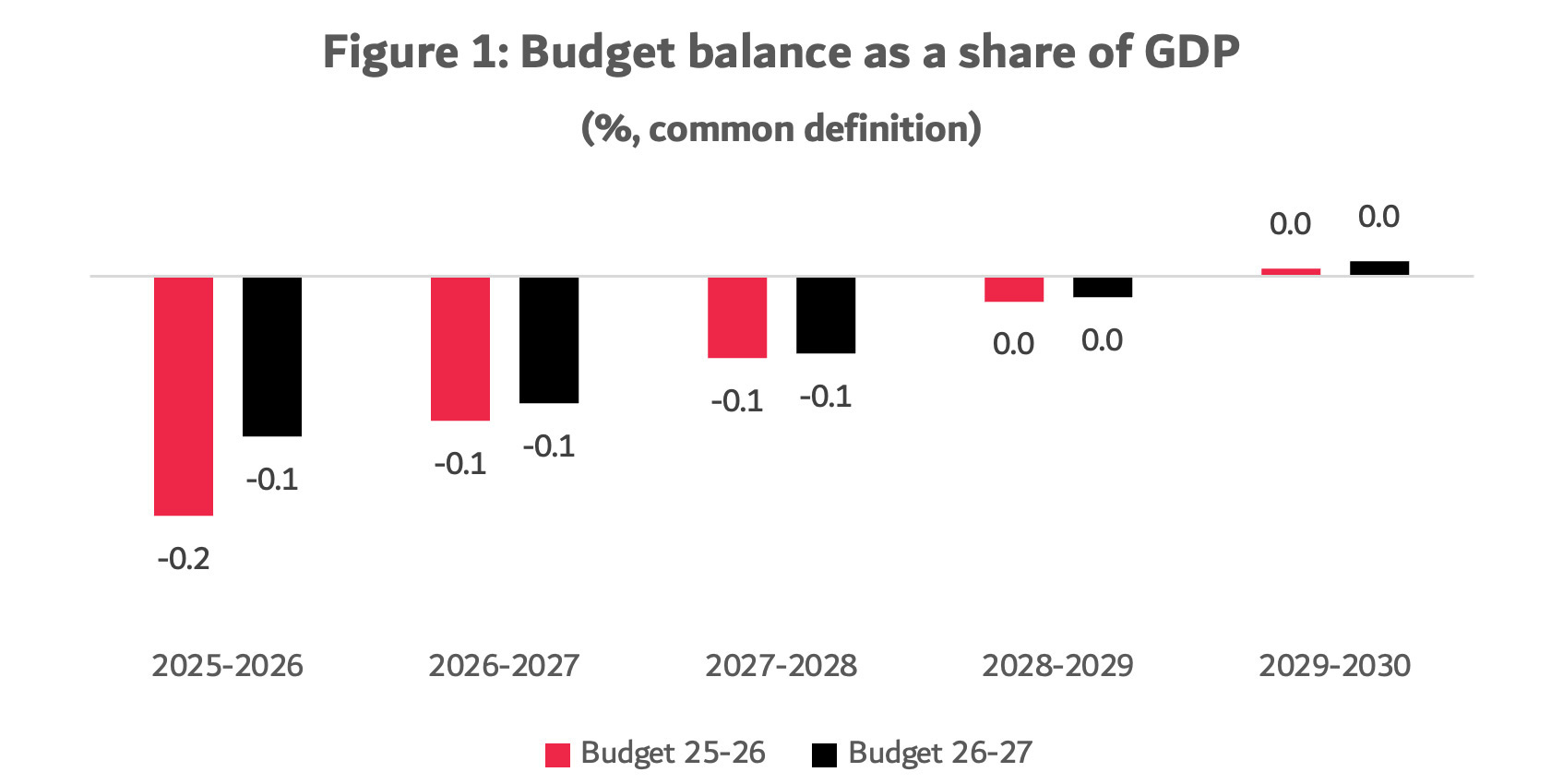

Québec’s balanced budget law has forced the government to focus on bringing back surpluses. Girard presented his five-year plan to do so in the previous budget. It included plans to reduce the growth of public spending, plans for crown corporations to bring in more revenue, changes to tax expenditures and a renewed plea for increased transfers from the federal government. Thanks to greater-than-expected revenue from taxes, the situation in this year’s budget is a little better than in the previous one, as shown in Figure 1.

The budget includes a limited number of new tax and spending measures totaling approximately 2B$ in 2026-2027. These include the yearly cost of a 3 per cent cap on the growth of the property school tax, subsidies for 5000 previously private childcare spots and funding to build 1000 affordable homes. The government also announced an automatic tax filing program similar to the one introduced by the federal government in its 2025-2026 budget last fall. The aims are the same: automatically filing taxes for individuals who may have not filed recently, so that they can be eligible for tax-provided income support. Revenu Québec, the province’s tax collection agency, has not yet specified the eligibility criteria or the delays of application for the new program. Pending changes to tax legislation, it will be in effect for tax year 2026.

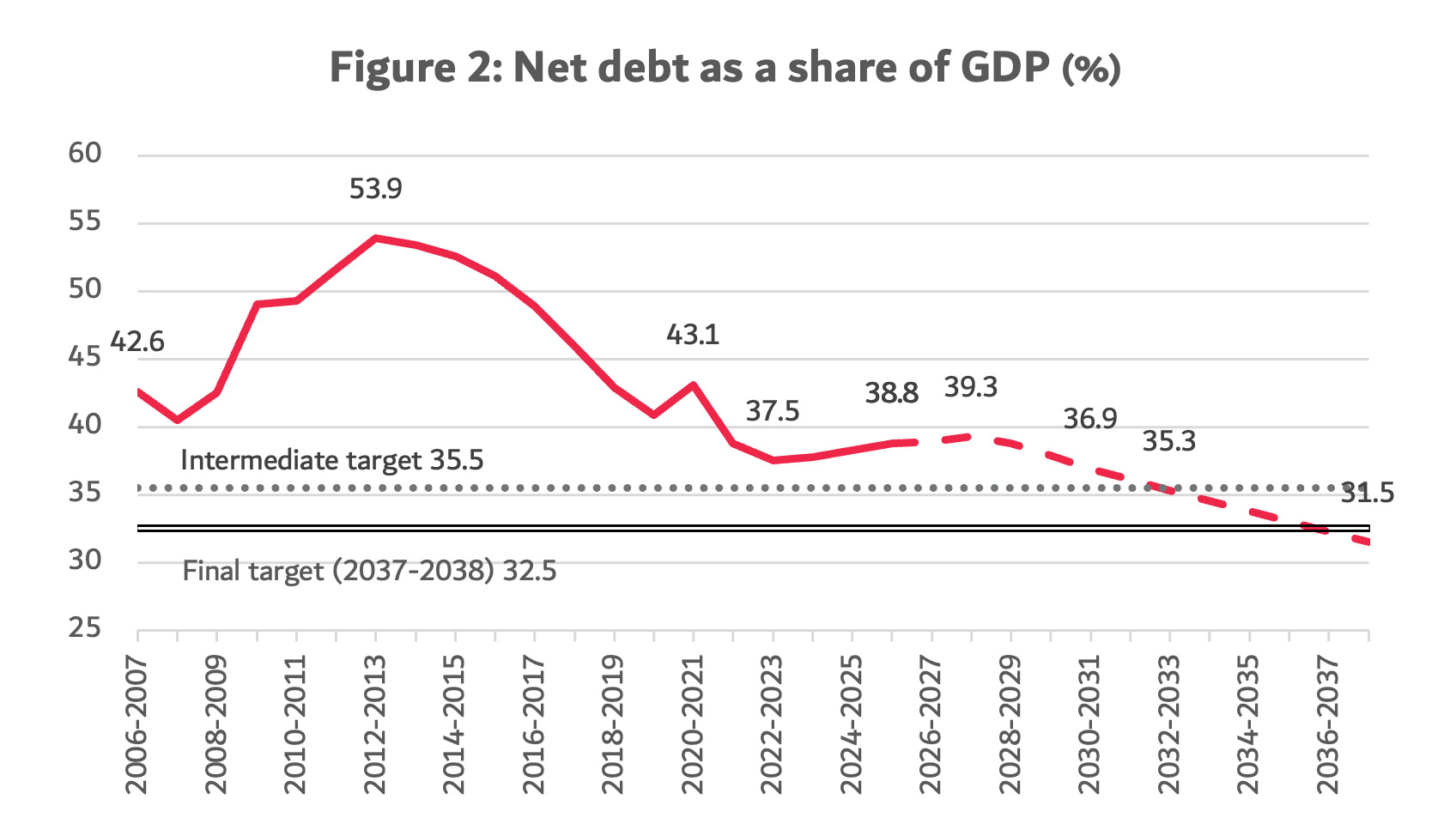

Québec also has a law that forces it to devote some of its budget to a sovereign wealth fund called the Generations Fund. The Fund’s objective is to reduce intergenerational inequality stemming from the province’s quickly aging population. That law dictates that the government’s net debt, including the assets of the Generations Fund, reaches a level of 35.5 per cent of GDP by 2032-2033 and 32.5 per cent in 2037-2038.

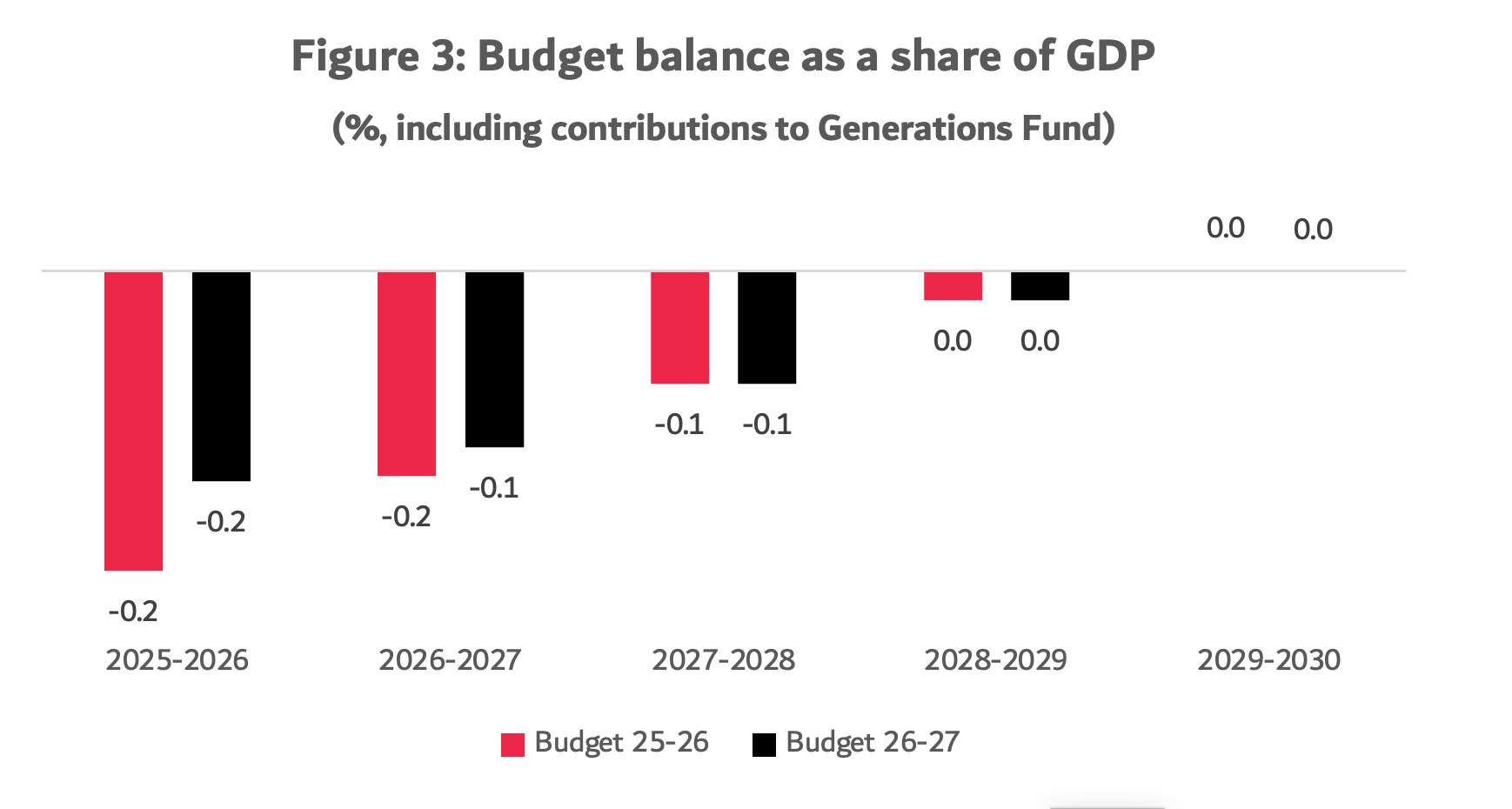

The government is still on track to reach these targets, if its plan to bring the budget back to balance succeeds. Figure 1 shows Québec’s budget balance according to the same definition used by other provinces and the federal government. However, the additional funding required for contributions to the Generations Fund means that the government needs to target an accounting surplus rather than simply a balanced budget, meaning that the funding gap is larger, as shown in Figure 3.

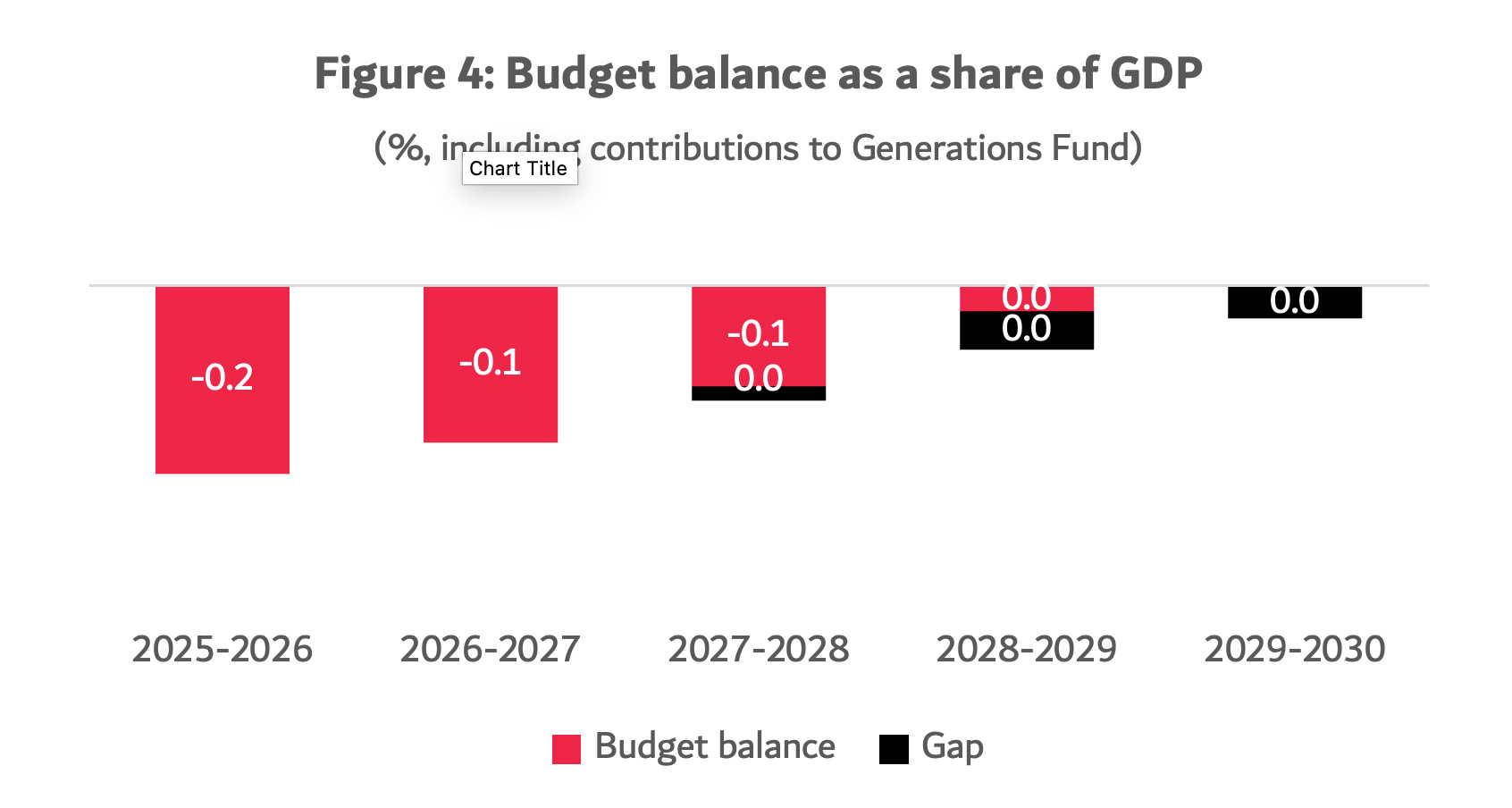

The biggest issue with Québec’s plan to bring its budget back to surpluses is that the government refuses to identify the necessary steps to reach the target in the last part of its five-year window. The plan presented last year contained “gaps to be bridged” worth up to 2.5B$ in years 27-28 to 29-30. These gaps have shrunk a bit in this year’s budget thanks to a higher baseline in 2025-2026 but the government still does not want to identify the added revenue or reduced spending that could bridge those gaps. The minister mentioned that the gaps might close on their own if the Canada-US-Mexico trade agreement is renewed and investment resumes thanks to the added certainty in the business climate.

Adding to the government’s challenge is the ongoing cost of existing programs. The expenditure budget, also presented on March 18th, highlights a funding gap of at least 0.23 percent of GDP in 2027-2028. This gap sits on top of the government’s current fiscal trajectory. That is, the government assumes that program spending will be below the costs of continuation for years after 2026-2027 and still has to find up to 0.33 percent of GDP in funding or cuts. This amounts to a 3.8B$ shortfall in 2028-2029. None of these issues are new. Since 2014, finance ministers have not explicitly committed funding that covers the costs of program continuation beyond the next financial year. They have frequently met that threshold, but they have never committed to doing so in advance.

These issues matter because the province is going into an election in a few months even as the global economic climate is still very unstable. Because the new premier will be sworn in after the budget, Girard has stated that the budget contains contingencies worth at least 250M$ a year for future spending plans, likely to be unveiled over the summer. After that, electoral politics will ramp up in earnest. Parties will compete with their tax and spending proposals for 2026 to 2030. And they will do so on top of an incomplete plan to bring the budget into balance after 3 years of deficits and expected cuts to the public service coming into force during the next premier’s first year. Winning next fall’s election may not be the victory every party savours!

Tax filing was supposed to be getting easier. That’s still a work in progress.

By Heather Scoffield | Originally published in The Toronto Star, March 7, 2026

It’s tax-filing season again, with all the headaches that brings for Canadians tearing apart their houses and their laptops to find the right paperwork before the deadline.

In theory, at least for low-income Canadians and the most vulnerable among us, the annual scramble should be getting easier. The federal government is starting to implement some changes announced in the last budget meant to automate filing for simple tax situations.

“It’s all about having access to the My CRA account, and using it,” says Elizabeth Mulholland, CEO of Prosper Canada, a charity dedicated to financial empowerment that helps low-income people across the country file their taxes.

But those changes are only inching along — even as the list of benefits, supports and financial information attached to proper tax filing is growing longer and longer.

More precious than T-4 forms or access to automatic filing, however, is what comes at the end of the dance with the Canada Revenue Agency: the notice of assessment — the document that summarizes your income and confirms how much you owe or are getting back in taxes.

It’s like a Golden Ticket — the key to unlocking federal and often provincial income support as well as trustworthy financial information about every taxpayer.

Without their notice of assessment, taxpayers rich and poor alike, will find it difficult, if not impossible, to access GST credits, caregiver credits, seniors’ benefits, help for groceries, space in your RRSP, your TFSA and your FHSA.

Acronyms aside, you’ll need your notice of assessment to get child benefits, dental benefits, workers benefits and disability benefits. In Ontario, you’ll need it to access social assistance.

There’s more, but you get the idea.

More and more, the notice of assessment is a linchpin to social service delivery at all levels, making it a crucial link in Canada’s social safety net.

But for those who need it most, it’s sometimes hard to get and easy to lose.

“It’s all about having access to the My CRA account, and using it,” says Elizabeth Mulholland, CEO of Prosper Canada, a charity dedicated to financial empowerment that helps low-income people across the country file their taxes.

No one should assume that such access is at everyone’s fingertips, especially if they are living in precarious circumstances. First, you need computer access, with Wi-Fi, and preferably with a secure connection. If you’re setting up an account, you also need identification, previous tax returns, and a steady address.

And let’s hope you don’t get locked out of your account. Getting back in can take several documents, and a password that may need to be sent by mail.

CRA and experts figure about 400,000 people are missing out on their benefits year after year because they’re not filing taxes.

That was the reason why last November, in Prime Minister Mark Carney’s first budget, the government announced a new initiative for automatic filing for low-income people with simple tax situations.

It has potential, but it’s rolling out gradually, and with some hiccups.

There are three different ways the CRA wants to make tax filing more automatic, but only one is ramping up right now, opening up on March 9 for this tax season: SimpleFile, an interactive digital or phone questionnaire which will be available to about 3 million people.

The system has been around for a while, but by invitation-only in the past, and uptake has been low. It’s more accessible this year.

This coming fall, CRA will launch a small pilot project to do “deemed filing” for low-income Canadians who haven’t filed their taxes at all, but should have.

And next March, CRA will start pre-filling tax returns for 1 million people, giving them a chance to approve the information before sending it in. The goal is to reach 5.5 million people by 2029.

The government is purposely moving cautiously so that it can understand the needs of vulnerable populations and consult along the way, says John Fragos, press secretary for the Office of the Minister of Finance and National Revenue.

In the meantime, low-income filers will lean heavily on community tax clinics staffed by trained volunteers, including about 700 chartered accountants in Ontario, and organized by charities like Prosper Canada. Same as it ever was.

“The word ‘automatic’ seems very misused,” says Lisa Rae, Prosper’s director of systems change.

Her frustration is that the federal government has been tossing around the automatic filing concept for years. But she’s hopeful that this time will be different.

Prosper Canada, along with the Maytree and Momentum organizations, are taking CRA’s offer to consult seriously and have designed ways to make the government plan more workable.

They argue that with more efficient use of the financial information the government already has, more formal exchanges of data with provincial governments, and a deeper understanding of the needs and financial flows of low-income people, CRA could catch up to other countries and develop a truly automatic system that would ensure almost $2 billion in unclaimed supports and benefits get into the hands of those who qualify.

Let’s hope the government is listening, and is on the way to making it truly easier for taxpayers of all kinds to find and keep that most-precious of all documents, the notice of assessment.

What history tells us about tax, trouble and the top one per cent

By Shirley Tillotson, Professor of history at Dalhousie University; expert advisor at the Canadian Tax Observatory | A version of this piece was originally published in the Halifax Examiner, February 25, 2026

Mark Carney wasn’t the only one making a splash in Davos. So were some 400 of the world’s millionaires and billionaires.

They were out in full force asking for governments to tax them more.

They know that governments everywhere need more revenue. Especially here in Canada where the turning-away-from-the-U.S. project set out by Prime Minister Carney will require billions in government spending on defence, infrastructure, and social supports.

Perhaps a tax on billionaire wealth (a simple one-off?) would be a good source of some of that money.

But the best tool at our disposal to raise this much-needed revenue is one we are set up already to use: income tax.

“But the income tax is a mess!” you say. Too complex and yet too ineffective at reaching high incomes. Worse, it scarcely touches wealth.

Yes. And yet. Let’s revisit the origins of the federal income taxes in North America. It’s a thought-provoking story of how an old tax, one crippled by many years of evasion, led to a fairer tax system.

The old tax was the municipal property tax. In many North American cities, including Toronto, Ottawa, and others in Ontario, property tax had become hopelessly corrupted.

Individual assessors took bribes, but worse, the municipalities attempted and increasingly failed to tax “personalty” – movable assets like jewellery, carriages, boats, and “intangible” assets, such as stocks and bonds.

The full scope of taxable personalty just wasn’t visible with the assessment tools of the day. So municipalities depended on the more easily “seen” homes and goods of the non-investing classes.

Federally, too, the poor, the farmer, and the modest earner paid a disproportionate share of their incomes on customs and excise taxation, the main source of national revenue.

From the 1880s onward, tax protesters clamoured and revolts brewed.

National and international grassroots movements called for taxation of inheritances and of land. Wealth, that is.

Worse, from most millionaires’ perspective, actual socialism was gaining electoral ground.

Public ownership! Confiscation! These were real possibilities.

In Canada, fabulously wealthy financier Isaak Walton Killam deplored how slow the feds were to adopt a war income tax. Finally, the one adopted in 1917 was modeled on the 1904 Ontario municipal income tax.

In this context, a well-ordered, mildly progressive-rate tax on upper incomes was, comparatively speaking, not a terrible threat.

By the 1910s, income tax on a national scale was looking like an easy way to spike the socialists’ guns, appease the fretful farmers, and soothe the tariff-oppressed consumer.

Its advocates, both rich and poor, could point to just such a tax that was working well in Ontario. A municipal income tax, on the books since 1866, was resuscitated in 1904, slightly revised, and used to correct for the inequity of the old property tax.

Income tax became a popular proposal for national tax reform, even among the very rich. The leading advocate, economist E.R.A. Seligman, came from a family of millionaire New York bankers.

In Canada, fabulously wealthy financier Isaak Walton Killam deplored how slow the feds were to adopt a war income tax. Finally, the one adopted in 1917 was modeled on the 1904 Ontario municipal income tax.

In the postwar debate, Killam was among those who insisted that the war income tax be continued.

Looking ahead to years of interest payments on the huge war debt, parliament agreed. They decided not to impose wealth taxes (a capital levy or a land value tax), but to keep the war income tax.

As MP William Foster Cockshutt, a millionaire industrialist, said in the House in 1919, he was willing, as all Canadians must be, “to submit to heavy taxation for some years to come.”

Like Seligman, both Cockshutt and Killam knew that, without direct taxation of substantial incomes, the nation’s tax structure was discredited, as the municipalities’ had been.

In 1919, with the recent revolution in Russia and labour revolts in Winnipeg and around the world, a nod to fairness, however modest, was in the interest of security of wealth.

It was not time to reform the polarizing, unreliable tariff. It was the time to do something that had proved feasible in Ontario: tax upper incomes.

Similarly, it is not time now to thoroughly reform our income tax system. It’s time to use familiar tools to do a few straightforward things, things that are widely seen as fair.

Raise the taxable percentage of capital gains. (Yes, try again.) Eliminate tax provisions that disproportionately benefit the top 1%. (Yes, try again.)

Do something. Or wait for the equivalent of 1919.

Rethinking Canada’s Tax System: What Works, What Doesn’t, What’s Next

Heather Scoffield | The Canadian Club of Toronto | February 24, 2026

The Canadian Club of Toronto hosted a panel on rethinking Canada’s tax system (what works, what doesn’t, what’s next), featuring the Canadian Tax Observatory’s Heather Scoffield, Deloitte’s Fatima Laher and the University of Calgary’s Jack Mintz. Moderated by Patrick Brethour of the Globe and Mail. Here’s a recording.

Heather Scoffield talks the U.S. Federal Reserve on TVO's The Rundown

Heather Scoffield | TVO's The Rundown | February 2, 2026

What happens to Canada’s approach to monetary policy when the world’s most powerful central bank, the U.S. Federal Reserve, is in turbulent times? Heather Scoffield breaks it down here for The Rundown on TVO.